0

Global dairy market risk assessment

All eyes on EU milk growth as seasonal peak approaches. EU milk supply growth is beginning to moderate following a period of exceptionally strong increases over recent months. EU milk collections were 3.6% higher in December 2017 compared to the previous year.

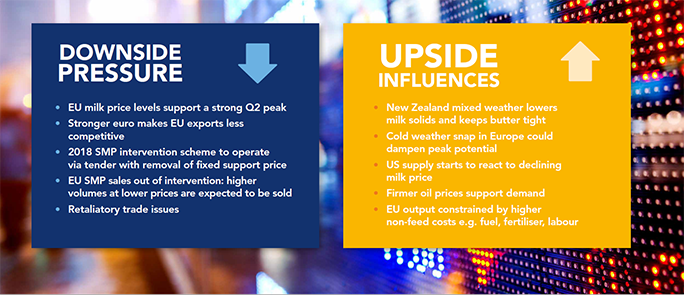

The cold weather front that swept across Europe in March may have further slowed milk growth – for a short period but weather is now normalising. Glanbia Ireland expects a strong milk production flush in Europe before current milk price cuts begin to stimulate a milk supply contraction by the third quarter of 2018.

US January 2018 milk production increased 1.8% year-over-year. The number came in above market expectations and was mainly driven by output growth in California.

New Zealand January 2018 milk collections were 4.9% lower as farmers experienced dry conditions across both islands, curbing milk production. However, the drop in milk output from New Zealand has been more than offset by higher milk deliveries in Europe.

EU butter prices ease after temporary spike higher

EU butter prices took the market by surprise by temporarily spiking higher in early February. This was mainly due to short-term tightness on physical deliveries ahead of strong demand profiles (Easter and Ramadan) with nervous buyers stepping-in to secure coverage.

Butter prices over the next number of months are expected to ease as milk and butter production increases but volatility is likely to remain a feature of the butter market.

Cheese markets remain firm

EU cheese prices are firm but the upcoming milk flush will see availability increase as more milk moves into cheese. Exchange rate fundamentals and further US dollar weakness in 2018 could favour US exports, particularly cheese in the Middle Eastern region.

SMP intervention stocks weigh on protein market

The outlook for SMP market remains very weak with further downside possible over coming months. 2018 SMP intervention scheme will operate via tender procedure which removes the fixed support price. More aggressive sales are expected by the EU Commission of existing SMP stocks out of intervention in 2018.

Protein prices are expected to remain weak with further downward pressure expected on rennet casein and milk protein concentrates.

At a macroeconomic level, global economic growth forecasts remain positive which are generally supportive to dairy consumption but the recent threats of retaliatory trade wars is concerning. Global dairy markets are expected to remain under pressure until there is a milk supply contraction which is not expected to occur before third quarter 2018.

GLOBAL DAIRY MARKET RISK ASSESSMENT

First Published 20 March 2018